3QFY2019 Result Update | IT

February 6, 2019

Tech Mahindra

NEUTRAL

CMP

`750

Performance Highlights

Target Price

-

(` cr)

3QFY19

2QFY19

% chg (qoq)

3QFY18

% chg (yoy)

Investment Period

12 Months

Net revenue

8,944

8,630

3.6

7,776

15.0

EBITDA

1,723

1,619

6.4

1,265

36.2

Stock Info

EBITDA margin (%)

19.3

18.8

50bps

16.3

300bps

Sector

IT

Adj. PAT

1,203

1,064

13.0

942

27.7

Market Cap (` cr)

73,597

Source: Company, Angel Research;

Net Debt (` cr)

(6,370)

Tech Mahindra posted good numbers for 3QFY2019 on all fronts. Revenues rose

Beta

0.7

3.5% qoq to end the period at US$1,261mn. On CC (constant currency) terms of

52 Week High / Low

780/564

the 4.3% qoq. In Rupee terms, revenues came in at `8,944cr v/s. `8,630cr in

Avg. Daily Volume

70,803

2QFY2019, up 3.6% qoq. On the operating front, the EBITDA margin came in at

Face Value (`)

5

19.3% v/s. 18.8% in 2QFY2019, a qoq expansion of 50bps. Consequently, PAT

BSE Sensex

36,617

came in at `1,203cr v/s. `1,064cr in 2QFY2019, a growth of 13.0% qoq. The stock

Nifty

10,934

has witnessed a good run-up and hence offer little upsides in near term;

Reuters Code

TEML.BO

hence, we maintain our neutral rating.

Bloomberg Code

TECHM@IN

Result highlights: Revenues rose 3.5% qoq to end the period at US$1,261mn.

Shareholding Pattern (%)

On CC (constant currency) terms of the 4.3% qoq. In Rupee terms, revenues

Promoters

35.9

came in at `8,944cr v/s. `8,630cr in 2QFY2019, up 3.6% qoq. The sales growth

MF / Banks / Indian Fls

14.8

during the quarter was broad based in terms of services, while in geographies it

FII / NRIs / OCBs

39.5

was USA and ROW, which drove the growth while Europe saw a moderate qoq

Indian Public / Others

9.8

growth. On the operating front, the EBITDA margin came in at 19.3% v/s. 18.8%

in 2QFY2019, a qoq expansion of 50bps. Consequently, PAT came in at `1,203cr

v/s. `1,064cr in 2QFY2019, a growth of 13.0% qoq.

Abs.(%)

3m 1yr

3yr

Sensex

4.8

5.4

48.7

Outlook and valuation: We expect a CAGR of 6.8% and 10.2% in USD and INR

Tech Mahindra

7.9

19.2

57.9

revenue respectively over FY2018-21E. The PAT is expected to grow at a

CAGR of 10.1% over FY2018-21E. We recommend our neutral rating.

Key financials (Consolidated, Indian GAAP)

3-year price chart

Y/E March (` cr)

FY2018

FY2019

FY2020E

FY2021E

Net sales

30,773

35,500

37,985

41,214

% chg

5.6

15.4

7.0

8.5

Net profit

3,800

4,498

4,693

5,072

% chg

35.1

18.4

4.3

8.1

EBITDA margin (%)

15.3

18.6

19.3

19.3

EPS (`)

43.0

50.9

53.1

57.4

P/E (x)

17.4

14.7

14.1

13.1

P/BV (x)

3.5

3.1

2.8

2.5

RoE (%)

20.2

21.2

19.8

19.2

Source: Company, Angel Research

RoCE (%)

15.4

20.7

21.1

20.9

EV/Sales (x)

2.3

2.0

1.9

1.7

Sarabjit kour Nangra

EV/EBITDA (x)

15.3

10.8

9.7

9.0

+91 22 3935 7800 Ext: 6806

Source: Company, Angel Research; Note: CMP as of February 5, 2019

Please refer to important disclosures at the end of this report

1

Tech Mahindra | 3QFY2019 Result Update

Exhibit 1: 3QFY2019 performance (Consolidated, Indian GAAP)

(` cr)

3QFY19

2QFY19

% chg (qoq)

3QFY18

% chg (yoy)

9MFY19

9MFY18

% chg (yoy)

Net revenue

8,944

8,630

3.6

7,776

15.0

25,850

22,718

13.8

Cost of revenue

5,985

5,692

5.1

5,381

11.2

13,201

12,479

5.8

Gross profit

2,959

2,938

0.7

2,395

23.5

12,649

10,240

23.5

SG&A expense

1,237

1,319

(6.2)

1,131

9.4

7,989

6,935

15.2

EBITDA

1,723

1,619

6.4

1,265

36.2

4,660

3,305

41.0

Dep. and amortization

284

294

(3.7)

274

3.4

859

786

9.2

EBIT

1,439

1,324

8.7

991

45.3

3,801

2,519

50.9

Interest

36

39

(7.7)

34

5.0

105

110

(4.2)

Other income

81

175

(54.0)

225

(64.2)

367

958

(61.7)

PBT

1,484

1,461

1.6

1,181

25.6

4,063

3,367

20.7

Income taxes

264

391

(32.6)

257

2.6

901

812

11.0

PAT

1,220

1,069

14.1

924

32.0

3,162

2,555

23.7

Minority interest

17

5

-

(19)

(3)

(22)

PAT after minority interest

1,203

1,064

13.0

943

27.5

3,165

2,578

22.8

Profit from associates

-

-

-

-

-

Exceptional item

-

-

-

-

-

Reported PAT

1,203

1,064

13.0

943

27.5

3,165

2,578

22.8

Adj. PAT

1,203

1,064

13.0

943

27.5

3,165

2,578

22.8

Diluted EPS

13.5

11.9

12.7

10.6

26.8

35.7

29.3

21.6

Gross margin (%)

33.1

34.0

(95)bps

30.8

228bps

48.9

45.1

386bps

EBITDA margin (%)

19.3

18.8

50bps

16.3

300bps

18.0

14.5

348bps

EBIT margin (%)

16.1

15.3

75bps

12.7

335bps

14.7

11.1

362bps

PAT margin (%)

13.4

12.3

112bps

12.1

132bps

12.2

11.3

90bps

Source: Company, Angel Research

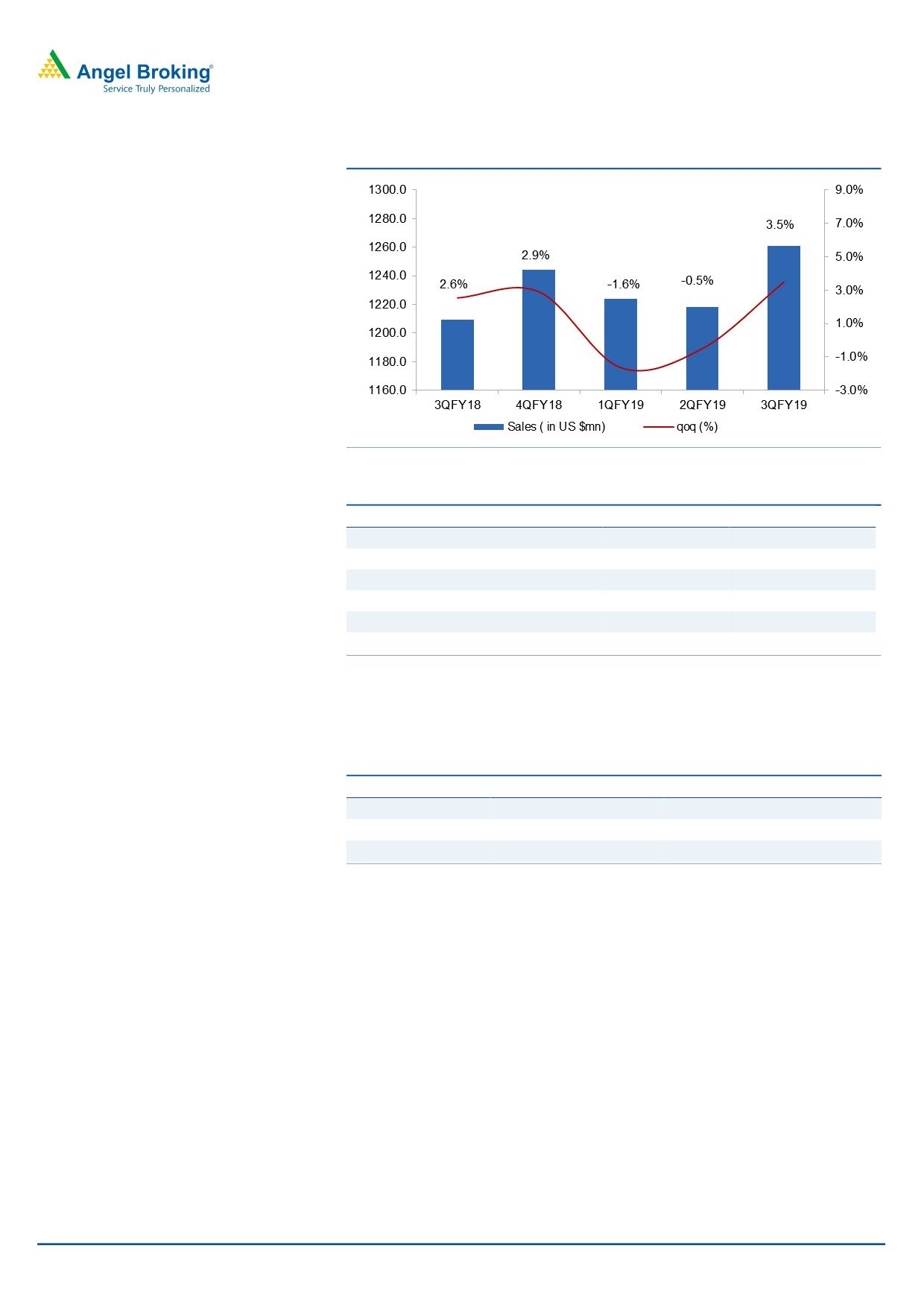

Revenue growth led by USA & ROW

For 3QFY2019, Tech Mahindra posted good set of numbers. Revenues rose 3.5%

qoq to end the period at US$1,261mn. On CC (constant currency) terms of the

4.3% qoq. In Rupee terms, revenues came in at `8,944cr v/s. `8,630cr in 2QFY2019,

up 3.6% qoq.

In terms of geography, USA constituted 47.4% of sales, a qoq growth of 4.4%,

while ROW was the key growth driver constituting 23.7% of sales, posting a qoq

growth of 4.8%. Europe, on the other hand posted a qoq growth of 1.0%.

In terms of the industries, the manufacturing came in at 20.5% of sales, posting

a qoq growth of 5.6% and was the main driver of growth. BFSI, which lead the

segment, contributing around 13.4% of sales, posting a qoq growth of 2.7%.

The key domain Retail, Transport & Logistics, posted a qoq growth of 6.7%. In

addition, the Technology, Media & Entertainment, posted a qoq de-growth of

0.8%. Communication, which is 41.1% of sales, posted a qoq growth of 2.5%.

In terms of services, growth continued to be led by BPO, which grew by 13.4%

qoq, while IT services grew by 2.8% qoq during the quarter. This is also reflected

in terms of the headcount, which has seen a steady rise in last three quarters V/s

flat or no additions in the IT services.

February 6, 2019

2

Tech Mahindra | 3QFY2019 Result Update

Exhibit 2: Trend in revenue growth

Source: Company, Angel Research

Exhibit 3: Growth in industry segments

Particulars

% to revenue

% growth (qoq)

Telecom

41.1

2.5

Manufacturing

20.5

5.6

TME

7.0

-0.8

BFSI

13.4

2.7

RTL

6.7

6.7

Others

11.3

4.4

Source: Company, Angel Research

In terms of geographies, ROW posted growth of 4.8% qoq, while Europe and US

posted a growth of 1.0% and 4.4% qoq respectively.

Exhibit 4: Growth trend in geographies

Particulars

% to revenue

% growth (qoq)

Americas

47.4

4.4

Europe

28.9

1.0

RoW

23.7

4.8

Source: Company, Angel Research

February 6, 2019

3

Tech Mahindra | 3QFY2019 Result Update

Hiring and client metrics

During the quarter, the company reported a net addition of 3,451 employees,

taking its overall headcount to 1,21,842. The BPO headcount currently stands at

43,439. Attrition (on LTM basis) was at 21%.

Exhibit 5: Employee metrics

Particulars

3QFY18

4QFY18

1QFY19

2QFY19

3QFY19

Software professionals

73,460

72,437

72,462

72,534

71,785

BPO professionals

35,496

34,190

34,700

39,407

43,439

Sales & support

6,180

6,180

6,390

6,450

6,618

Total employees

1,12,886

1,12,807

1,13,552

1,18,391

1,21,842

Attritions (%)

17

18

19

20

21

Source: Company, Angel Research

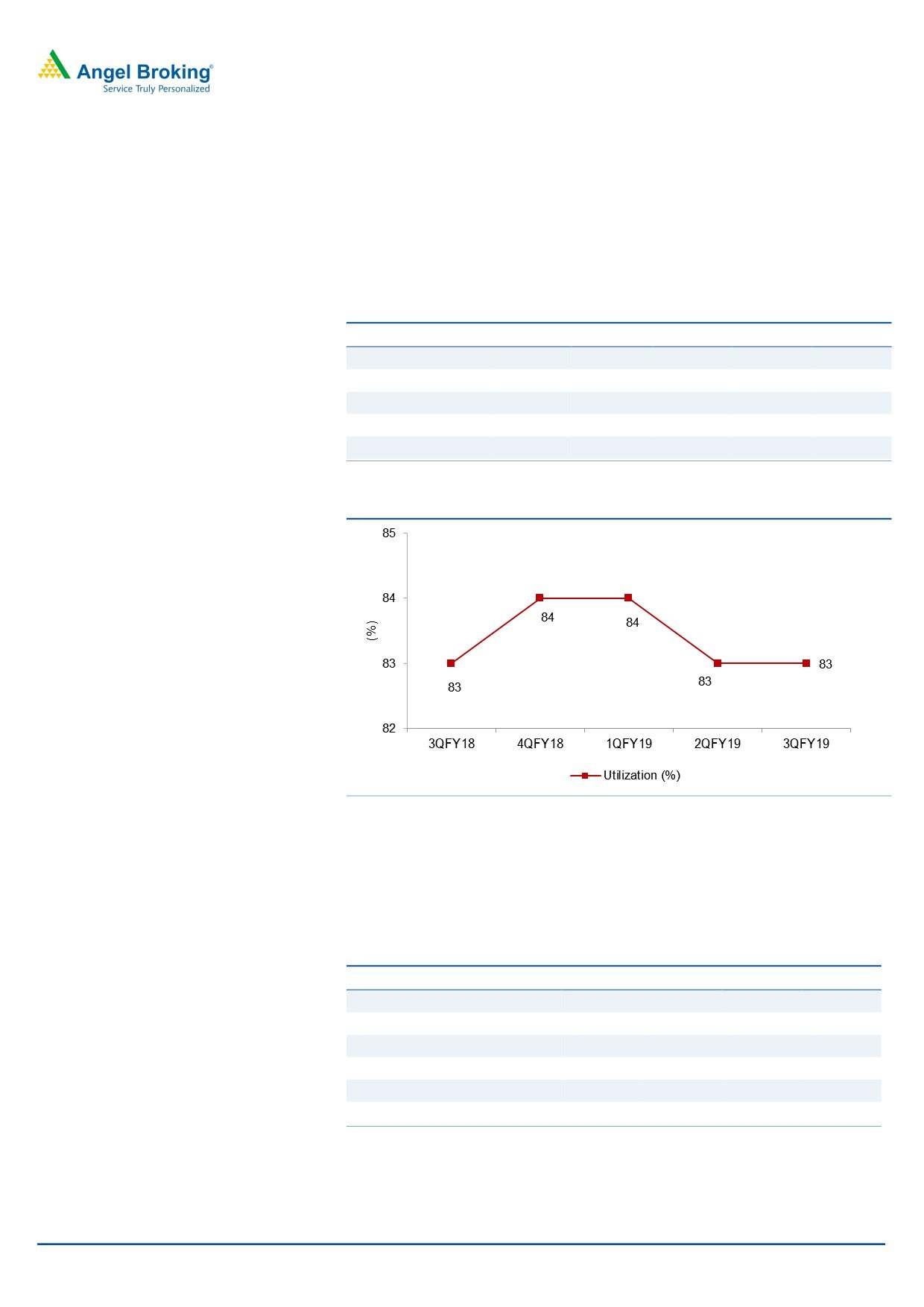

Exhibit 6: Trend in utilization rate

Source: Company, Angel Research

On the client additions front, the company added 5 clients. One client each was

added in the more than US$20mn and US$50mn each. In addition, in terms of the

growth drivers, the main driver has been client additions during the quarter, with

repeat business contributing 94.6% v/s. 97.4% in 2QFY2019.

Exhibit 7: Client metrics

Particulars

3QFY18

4QFY18

1QFY19

2QFY19

3QFY19

Total active clients

903

913

926

930

935

US$1mn-5mn

235

236

242

250

259

US$5mn-10mn

71

71

68

71

69

US$10mn-20mn

43

41

39

41

42

US$20mn-50mn

24

24

31

28

28

US$50mn+

16

16

16

17

18

Source: Company, Angel Research

February 6, 2019

4

Tech Mahindra | 3QFY2019 Result Update

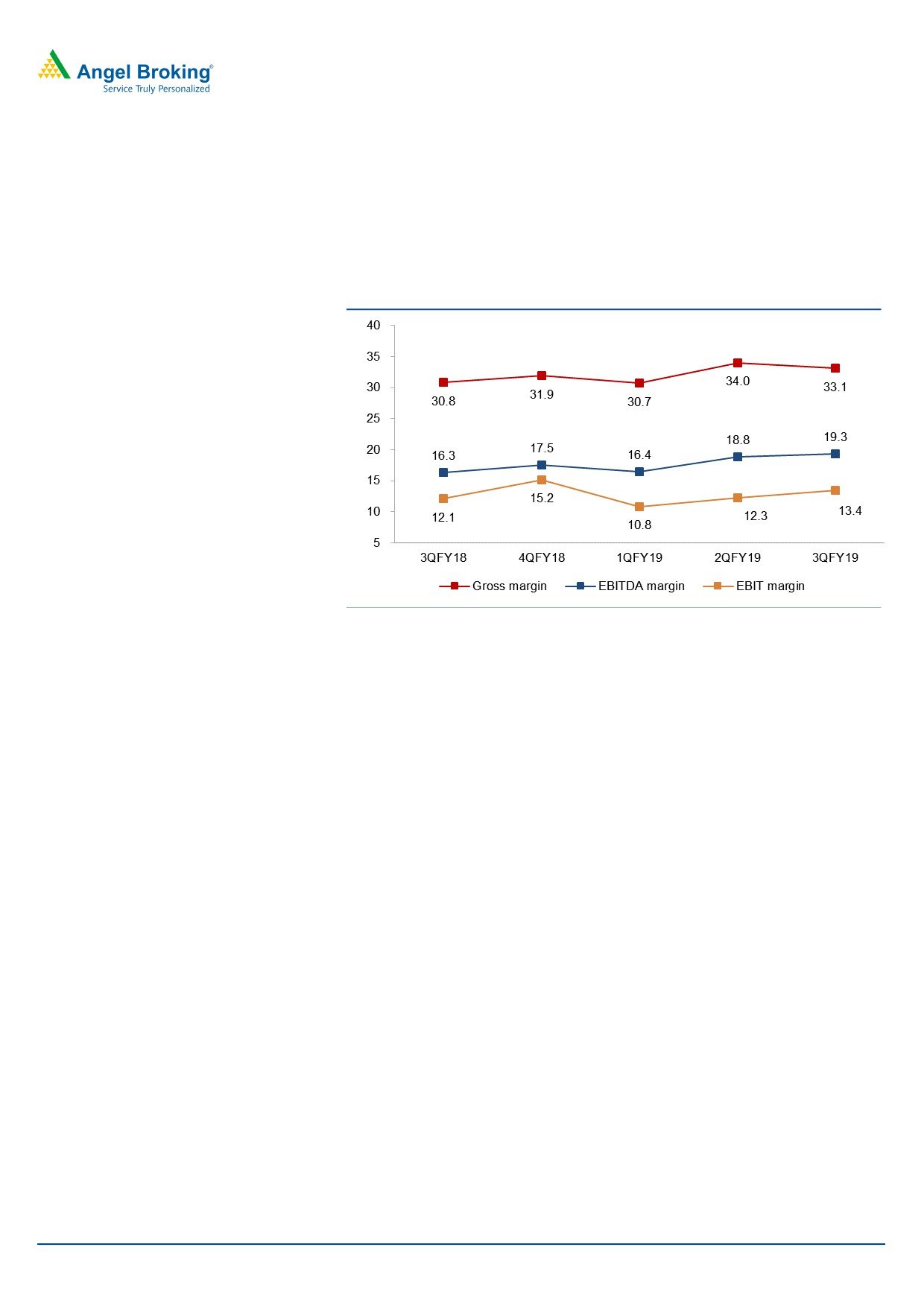

Operating margin expands

On the operating front, the utilization levels during the quarter came in at 82%

v/s. 81% in 2QFY2019, which along with volumes also aided the margins to come

in higher. On the operating front, the EBITDA margin came in at 19.3% v/s. 18.8%

in 2QFY2019, a qoq expansion of 50bps.

Exhibit 8: Margin trend (%)

Source: Company, Angel Research

Investment arguments

Growth prospects decent: Over the last one year, the IT services of the company

has just about been decent one, as reflected by the 9MFY2019 performance;

where the segment has posted a 12.8% yoy, while BPO which has seen robust

additions has witnessed a yoy growth of 26.3%. In addition, its main industry

Communication did not witnessed much growth during the year, while the growth

was much driven by the manufacturing & TEM space. Thus unlike large players

which benefit from the uptick in the growth in the Industry; Tech Mahindra; on a

best case scenario just matches the Industry growth and depends on the

Telecommunication spends. Thus in near term the company is depended on the

5G spends which are expected to come out by 2020 and mostly likely reflect by

FY2021. Thus, on a medium term, the company might just match the Industry

growth; however, concerns over long-term drivers to sustain the growth

organically persists.

Operating performance on an uptick: On the margin front, improvement, on

the back of synergies and productivity gains has started reflecting from

2QFY2018. Company has continued its margin recovery since then. For 3QFY2019,

the company posted margins of 19.3% on EBDITA affront from 14.4% in FY2017.

While there are still levers in terms, of the improved business mix, uptick in deal

size and productivity, however given the near term, pressures on employee cost

where tech Mahindra is at risk given the high onsite mix, we expect up moves

from heron to be gradual.

February 6, 2019

5

Tech Mahindra | 3QFY2019 Result Update

Outlook and valuation

We expect a CAGR of 6.8% and 10.2% in USD and INR revenue respectively

over FY2018-21E. The PAT is expected to grow at a CAGR of 10.1% over

FY2018-21E. while the stock has moved up in anticipation of a good uptick in

the communication segment supported by the upcoming 5G opportunity; we

view this opportunity cautiously and believe that given that the core IT

services business of the company is not growing as well as large peers; could

risk the stock performance going forward. Even after factoring a decent uptick

in the sales growth during FY2020-21E, we find that upsides at 14xFY2020E

would be limited, We recommend our neutral rating.

Exhibit 9: Key assumptions

FY2020E

FY2021E

Revenue growth (US$)

7.0

8.5

USD-INR rate (realized)

71.0

71.0

Revenue growth (`)

7.0

8.5

EBITDA margin (%)

19.3

19.3

Tax rate (%)

25.0

25.0

EPS growth (%)

4.3

8.1

Source: Company, Angel Research

Company Background

Tech Mahindra was founded in 1986 as a joint venture between Mahindra Group

and British Telecom (BT) to service the latter. Later on, the company started

servicing other external clients as well (solely in the telecom industry). In June

2009, Tech Mahindra acquired a 42.7% stake in erstwhile Satyam Computers (now

Mahindra Satyam) and now the latter is entirely merged with the company. The

company acquired the companies - LCC and Softgen. These two acquisitions have

been consolidated in 4QFY2015. LCC is one of the world’s largest independent

global providers of network engineering services to the telecommunications

industry. LCC is estimated to have annual revenues of more than US$400mn

(CY2014), with workforce of over

5,700 network professionals across five

continents and more than 50 countries.

February 6, 2019

6

Tech Mahindra | 3QFY2019 Result Update

Profit and loss statement (Consolidated, Indian GAAP)

Y/E March (` cr)

FY2017 FY2018 FY2019 FY2020E FY2021E

Net sales

29,141

30,773

35,500

37,985

41,214

Cost of revenues

20,566

21,530

23,785

25,070

27,201

Gross profit

8,575

9,243

11,715

12,915

14,013

% of net sales

29.4

30.0

33.0

34.0

34.0

SG&A expenses

4,390

4,533

5,112

5,584

6,058

% of net sales

15.1

14.7

14.4

14.7

14.7

EBITDA

4,184

4,710

6,603

7,331

7,954

% of net sales

14.4

15.3

18.6

19.3

19.3

Depreciation and amortization

978

1085

1243

1329

1442

% of net sales

3.4

3.5

3.5

3.5

3.5

EBIT

3,206

3,625

5,361

6,002

6,512

% of net sales

11.0

11.8

15.1

15.8

15.8

Interest expense

129

162

162

162

162

Other inc., net of forex gain/(loss)

778

1,417

481

481

481

Profit before tax

3,855

4,879

5,679

6,320

6,830

Provision for tax

1,002

1,093

1,136

1,580

1,708

% of PBT

26.0

22.4

20.0

25.0

25.0

PAT

2,853

3,786

4,543

4,740

5,123

Exceptional item

-

-

-

-

-

Minority interest

40

(14)

45

47

51

Reported PAT

2,813

3,800

4,498

4,693

5,072

Adjusted PAT

2,813

3,800

4,498

4,693

5,072

Fully diluted EPS (`)

32.1

43.0

50.9

53.1

57.4

February 6, 2019

7

Tech Mahindra | 3QFY2019 Result Update

Balance sheet (Consolidated, Indian GAAP)

Y/E March (` cr)

FY2017

FY2018

FY2019 FY2020E FY2021E

Equity capital

439

442

442

442

442

Preference capital

-

-

-

-

-

Share premium

-

-

-

-

-

Profit and loss

15,998

18,401

20,794

23,291

25,989

Other reserves

0

-

-

-

-

Net worth

16,438

18,843

21,236

23,732

26,430

Secured loans

1,219

1,726

1,726

1,726

1,726

Unsecured loans

-

-

-

-

-

Total debt

1,219

1,726

1,726

1,726

1,726

Other long term liability

537

537

537

537

537

Long-term provisions

620

555

555

555

555

Minority interest

464

509

555

602

653

Amount pending investigation

1,230

1,300

1,300

1,300

1,300

Total capital employed

20,508

23,469

25,908

28,452

31,201

Gross block

11,677

13,924

14,924

15,924

16,924

Accumulated dep.

(5,217)

(6,302)

(7,545)

(8,874)

(10,317)

Net block

6,460

7,622

7,380

7,050

6,608

Capital WIP

373

240

240

240

240

Total fixed assets

6,833

7,862

7,620

7,290

6,848

Investments

2,396

4,691

9,636

13,054

16,733

Long term loans and adv.

2,435

2,646

3,117

3,118

3,119

Interest in TML benefit trust

-

-

-

-

-

Deferred tax asset, net

267

571

571

571

571

Other non-current assets

0

-

-

-

-

Inventories

61

66

66

66

66

Sundry debtors

5,338

6,498

7,136

7,521

8,160

Cash and cash equv.

3,219

3,044

4,000

3,900

3,841

Loans and advances

5,518

5,054

5,054

5,051

5,048

Current investments

-

-

-

-

-

Unbilled revenue

-

-

-

-

-

Sundry creditors

(2,312)

(6,559)

(10,828)

(11,585)

(12,570)

Other liabilities

(2,860)

(403)

(463)

(533)

(613)

Provision

(387)

-

-

-

-

Working capital

8,577

7,700

4,964

4,419

3,931

Total capital deployed

20,508

23,469

25,908

28,452

31,201

February 6, 2019

8

Tech Mahindra | 3QFY2019 Result Update

Cash flow statement (Consolidated, Indian GAAP)

Y/E March (` cr)

FY2017

FY2018

FY2019

FY2020E FY2021E

Pretax profit from operations

2,853

3,786

4,543

4,740

5,123

Depreciation

978

1,085

1,243

1,329

1,442

Exp. (deffered)/written off/others

-

-

-

-

1

Pre tax cash from operations

3,831

4,871

5,786

6,070

6,566

Other income/prior period ad

778

1,417

481

481

481

Net cash from operations

4,609

6,288

6,267

6,551

7,047

Tax

(1,002)

(1,093)

(1,136)

(1,580)

(1,708)

Cash profits

3,607

5,195

5,131

4,971

5,340

(Inc)/dec in

Sundry Debtors

433

(1,160)

(638)

(386)

(639)

Inventories

(21)

(5)

-

-

-

Loans and advances

(1,485)

464

-

3

3

Sundry creditors

36

4,247

4,269

758

985

Others

660

(2,457)

60

70

80

Net trade working capital

(377)

1,089

3,692

445

429

Cashflow from operating activities

3,230

6,284

8,823

5,416

5,768

(Inc)/dec in fixed assets

(1,840)

(1,029)

243

329

442

(Inc)/dec in investments

(1,153)

(2,295)

(4,945)

(3,418)

(3,679)

(Inc)/dec in other non-current assets

0

0

-

-

-

Cashflow from investing activities

(2,992)

(3,324)

(4,703)

(3,088)

(3,237)

Inc/(dec) in debt

(217)

(507)

-

-

-

Inc/(dec) in deferred revenue

-

-

-

-

-

Inc/(dec) in equity/premium

-

0

-

-

-

Inc/(dec) in minority interest

(271)

(45)

(45)

(47)

(51)

Dividends

(924)

(1,447)

(2,105)

(2,196)

(2,373)

Others

376

(1,136)

(1,015)

(186)

(170)

Cashflow from financing activities

(1,037)

(3,134)

(3,164)

(2,428)

(2,592)

Cash generated/(utilised)

(800)

(174)

955

(100)

(60)

Cash at start of the year

4,018

3,219

3,044

4,000

3,900

Cash at end of the year

3219

3044

4000

3900

3841

February 6, 2019

9

Tech Mahindra | 3QFY2019 Result Update

Key Ratios

Y/E March

FY2017

FY2018

FY2019

FY2020E

FY2021E

Valuation ratio (x)

P/E (on FDEPS)

23.4

17.4

14.7

14.1

13.1

P/CEPS

17.4

13.6

11.5

11.0

10.2

P/BVPS

4.0

3.5

3.1

2.8

2.5

Dividend yield (%)

1.2

1.9

2.7

2.8

3.1

EV/Sales

2.5

2.3

2.0

1.9

1.7

EV/EBITDA

17.1

15.3

10.8

9.7

9.0

EV/Total assets

10.5

9.2

9.4

9.8

10.4

Per share data (`)

EPS

32.1

43.0

50.9

53.1

57.4

Cash EPS

43.2

55.3

65.0

68.2

73.7

Dividend

9.0

14.0

20.4

21.2

23.0

Book value

187.3

213.3

240.4

268.6

299.2

Dupont analysis

Tax retention ratio (PAT/PBT)

0.7

0.8

0.8

0.7

0.7

Cost of debt (PBT/EBIT)

1.2

1.3

1.1

1.1

1.0

EBIT margin (EBIT/Sales)

0.1

0.1

0.2

0.2

0.2

Asset turnover ratio (Sales/Assets)

4.3

3.9

4.7

5.2

6.0

Leverage ratio (Assets/Equity)

0.4

0.4

0.4

0.3

0.3

Operating ROE (%)

17.1

20.2

21.2

19.8

19.2

Return ratios (%)

RoCE (pre-tax)

15.6

15.4

20.7

21.1

20.9

Angel RoIC

19.0

18.0

24.7

24.7

24.0

RoE

17.1

20.2

21.2

19.8

19.2

Turnover ratios( x)

Asset turnover (fixed assets)

4.3

3.9

4.7

5.2

6.0

Receivables days

70

79

79

75

75

Payable days

30

80

119

115

116

February 6, 2019

10

Tech Mahindra | 3QFY2019 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited, Metropolitan Stock Exchange Limited, Multi Commodity Exchange of India Ltd and National

Commodity & Derivatives Exchange Ltd It is also registered as a Depository Participant with CDSL and Portfolio Manager and

Investment Adviser with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Limited is a registered

entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number INH000000164.

Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in

securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public offering of

securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate

the contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this

report. Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we

cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this

document. While Angel Broking Limited endeavors to update on a reasonable basis the information discussed in this material, there

may be regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or

in connection with the use of this information.

Disclosure of Interest Statement

Tech Mahindra

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or

No

relatives

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

February 6, 2019

11